Red Flag Alert – Caffeine Jitters

Red Flag Alert – Caffeine Jitters

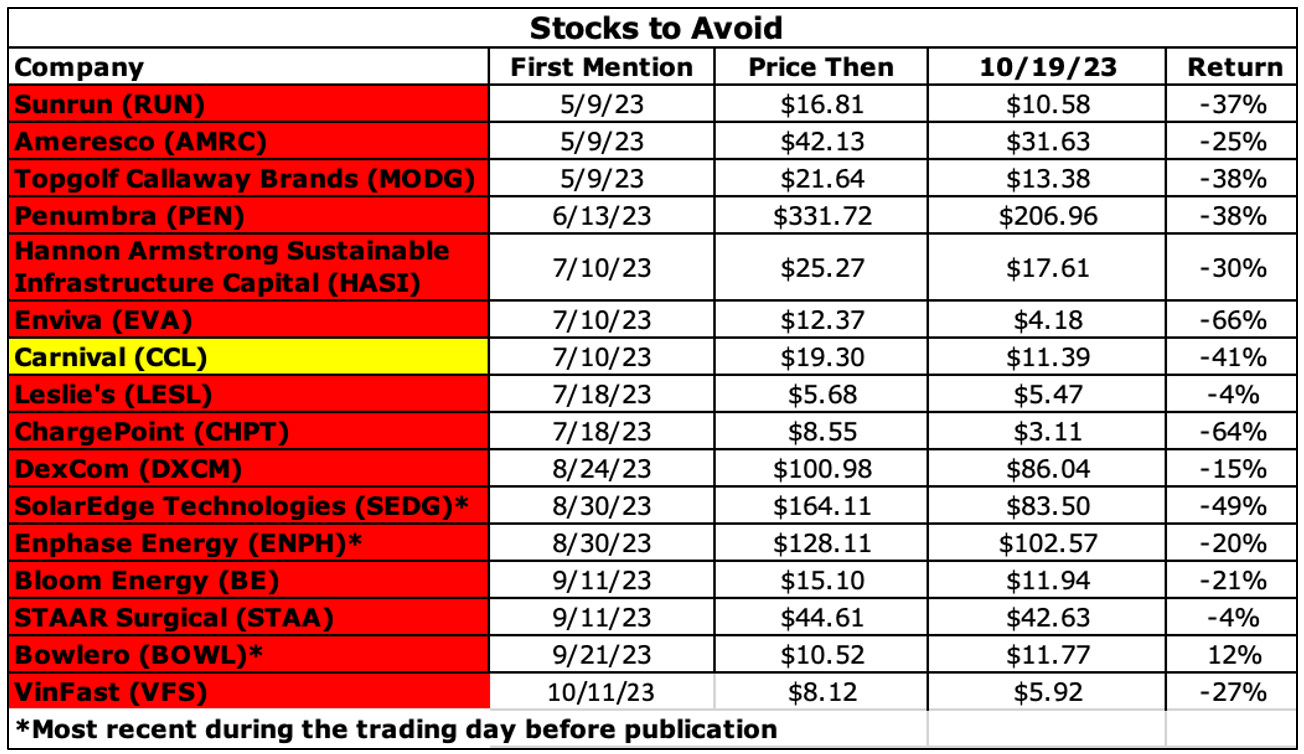

Plus Updates and Master List of Stocks to Avoid

New – Dutch Bros Among the ‘Financially Fragile’

Update – SolarEdge, Enphase Get Burned

Update – More Fun and Games with Bowlero

Bonus – Latest Master List of Stocks to Avoid

From the “eyes bigger than their stomach” department...

It’s one thing to have a good concept, it’s another to be able to afford it...

Therein lies the problem with Dutch Bros. (BROS), the rapidly growing drive-through coffee chain.

The company has been showing up for months on the “unattractive debt list” published by my friends at Kailash Concepts (KCR). That’s a list that shows companies with rising debt and without enough earnings to cover it.

By virtue of being on that list, it also landed on KCR’s list of 153 “financially fragile” companies with market caps above $500 million that rank in the bottom third of those whose operating earnings can’t cover their interest rate expense.

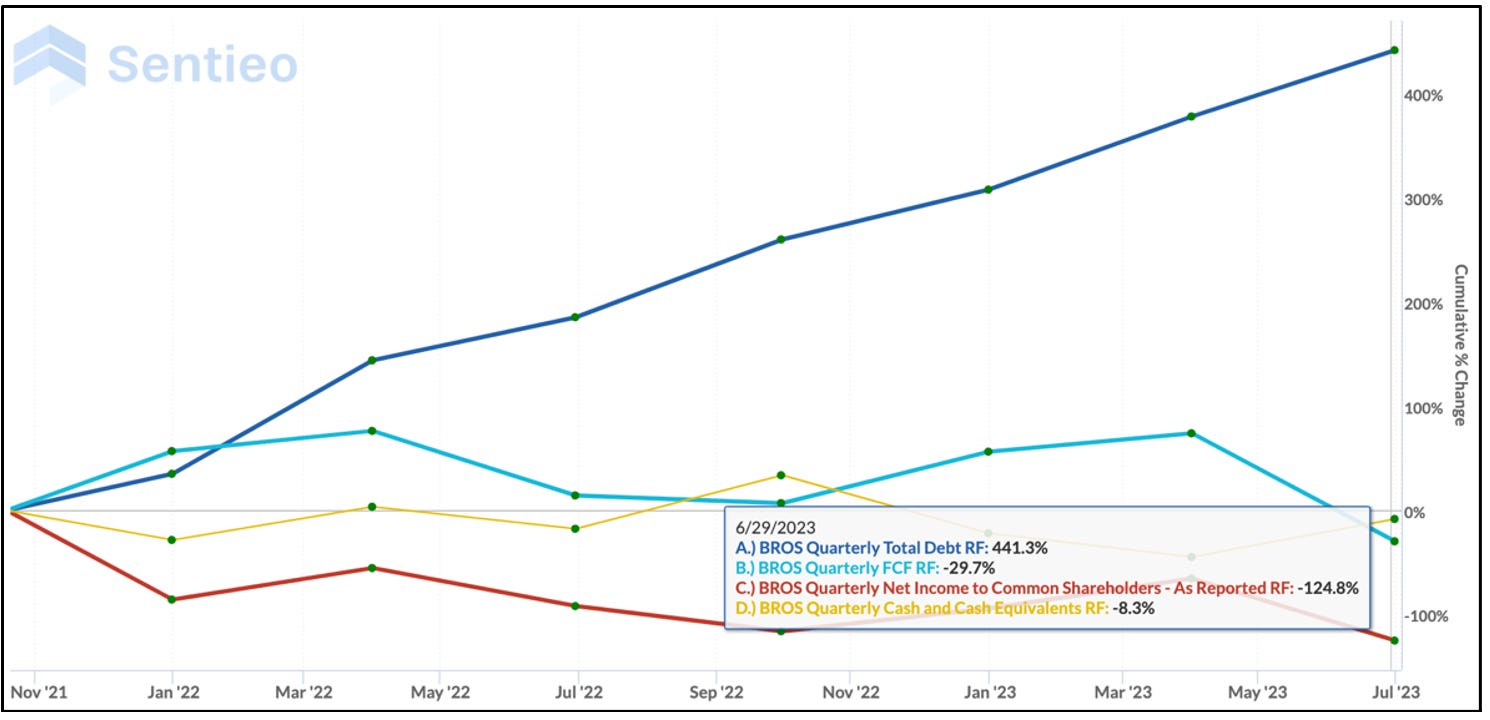

That story is in the chart below...

Debt (blue line) over the past two years has shot higher, while free cash flow (turquoise), cash (yellow) and net earnings (red) have trended lower.

That’s not a good combo…

Especially not good for a company that has dangled an aggressive growth path in front of Wall Street since its IPO... perhaps too aggressive.

Since its 2021 IPO, when it had just 471 stores in 11 states, the company actively talked about how it believed it could balloon to 4,000 units....

It never said when that would happen.

Now it does, saying it will take somewhere between 10 and 15 years.

As we all know, those targets are meaningless... they’re steeped in little more than aspiration, almost out of whole cloth for most companies. That’s especially true for Dutch Bros, given its need to secure drive-through locations... not necessarily the easiest thing to do. (I questioned the long-term target and the drive-through risk two years ago in a piece headlined, “One Under-Appreciated Risk of the Dutch Bros Hot IPO”.)

And that was before interest rates shot higher.

Now a high-growth model is a high-stakes game in a high-interest rate market...

In a mere two years, the company’s store count has shot up by 60% to 754 stores in 14 states, and its stock has lost roughly half its value (considerably more from its highs.)

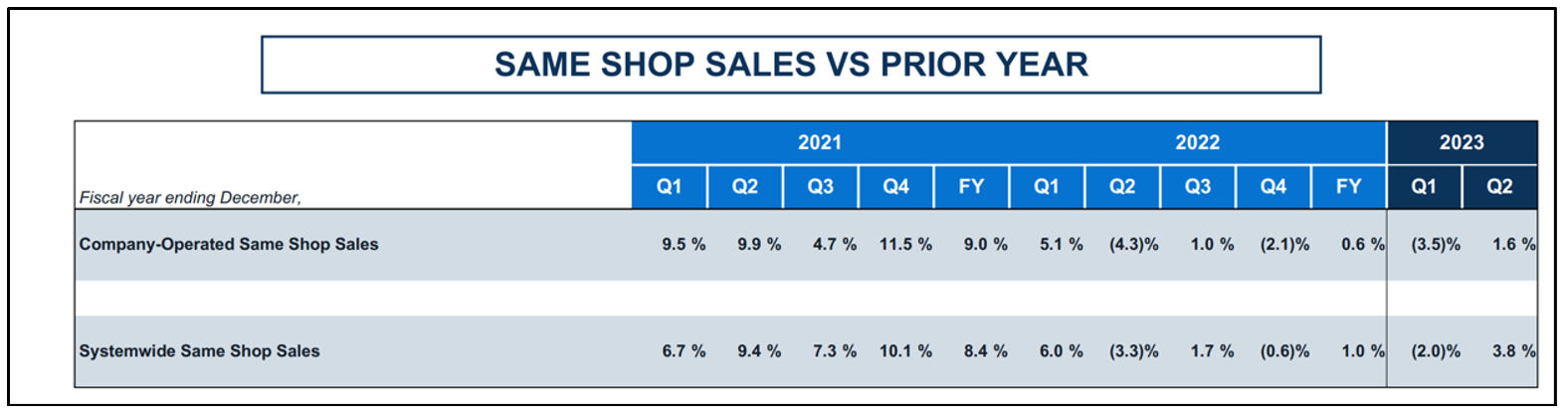

That shouldn’t be too surprising, given the company’s performance, with same-store sales not just erratic, but sputtering.

Here’s the thing...

By now it would seem the company should routinely be showing positive net income and positive operating cash flow... enough to start self-financing its growth, with maybe a line of credit to fill in the gaps.

But restaurant consultant (and my pal) John Gordon of Pacific Management Consulting Group says the company is hamstrung because of its approach to building new territories, using a concept called “fortressing.”

That means going into a market like Sacramento “and buying everything available,” John says. “The logic is that they’re preventing anybody else from coming in.”

Dominoes may be the fortressing king, and it works well because they’re using franchisees to expand.

But as John explains, Dutch Bros’ franchising has been “on deep freeze for several years, and the BROS expansion is only really via company units.”

In other words, “it’s not other people’s money at risk, it is corporate money at risk. And it’s why BROS new store Capex requirements are outstretching free cash flow available.”

And it’s why the company recently did a stock offering that diluted existing shareholders...

Even though it’s making money at the store level, it needs cash and simply can’t keep piling on more debt.

The good news for Dutch Bros is that its brand is well-established…

The bad... it has gotten itself boxed in as a “fast-growth” story with its absurd “4,000” store target.

Yet, if you talk to restaurant experts like John, it “needs to get its capital development plan aligned to meet the cash flow that they actually have.”

With a new CEO Christine Barone taking over the reins in January, perhaps things will change. She has an exceptional pedigree, and investors often given new leaders a grace period to prove themselves. (Just as they did Mary Dillon when she moved to Foot Locker (FL) after a successful run at Ulta Beauty (ULTA). Then reality took over.)

During that honeymoon, the stock very well could rise, as they did at Foot Locker...

But with Dutch Bros, given its balance sheet, it would appear that something has to give. That very well could translate into slowing store growth will likely slow... and so will Wall Street expectations.

For that reason, even with its stock as blasted as it has been, Dutch Bros gets a Red Flag. There are simply better stocks to own.

Moving on, time for a few updates, but before we do....

Below is an update of the Red Flag Alerts (RFA)...

The concept behind RFA is stocks to avoid. They don’t usually move this fast, but this is that kind of market.... the kind when, if you’re an investor as opposed to a trader, it pays to stick with quality.

Speaking of which, a few updates...

SolarEdge (SEDG) warned last night that demand in Europe was unexpectedly weak. That was part of the reason I red flagged it in August along with rival Enphase (ENPH). SolarEdge’s news isn’t likely to bode well for rival Enphase, whose biggest growth market is Europe.

Since then, SolarEdge has lost roughly 50% of its value; Enphase, 20%. Even with these declines, these stocks are still well above their pre-pandemic levels… when business was nowhere near what it was post-pandemic.

Yet it would seem, earnings risk sliding back to pre-pandemic levels.

Between here and there, traders may very well have a field day. There are better options for investors.

Bowlero’s (BOWL) stock has been like a bouncing bowling ball since I first red-flagged it, but it’s popping considerably higher on news that it’s raising $433 million through a sale-leaseback with VICI Properties.

Bowlero will no doubt use the cash to buy more bowling alleys... and a sale-leaseback is cheaper than adding more debt to its growing pile, whose interest rate is hovering at close to 8.65%.

But just remember: Anytime a company has to resort to alternative financing, investors should be on guard. I have no doubt this stock will have a life of its own, especially if and as short-sellers cover their position.

But if that happens, watch out. Other than getting more money to do more deals, nothing has changed. “Think of it like an option: They extended the expiration date,” says one friend, adding: “Big Lots did this and it stock doubled before falling 50%.”

Between here and there, traders may very well have a field day. There are better options for investors.

Reminder, if you like what you read please click the heart below and tell your friends and neighbors!

DISCLAIMER: This is solely my opinion based on my observations and interpretations of events, based on published facts and filings, and should not be construed as personal investment advice. (Because it isn’t!)

Feel free to contact me at herbgreenberg@substack.com. You can follow me on Twitter and Threads @herbgreenberg.

Great analysis on Dutch Bros, Herb. Definitely a red flag, imo too. Out of curiosity, what is your rationale for Dexcom being a red flag?

Hey herb…hope yur feeling good …know u many years …thanks for sharing …love “caffeine jitters” concept