Red Flag Alert – Sign of the Times

Red Flag Alert – Sign of the Times

The paradoxical battleground known as Marathon Digital

When I started Red Flag alerts, I made it clear the focus was stocks to avoid, not stocks to short. (Unless you’re a short seller, that is, who understands the risks. And even then...)

That said, the concept of easy- and hard-to-short stocks can provide a window into stocks that could be vulnerable to sharp run-ups – even if they don’t deserve it... and then, possibly falling off a cliff.

A great example is bitcoin miner Marathon Digital Holdings...

As one friend in my network put it...

No borrow available in January 2023 with a 100% cost to borrow.

Now millions available and no cost to borrow.

Quick Shorting Primer

Shorting involves borrowing shares, and then immediately selling them, with hopes if all goes right of buying them back at a lower price. If the “borrow,” as they call it, is tight, the so-called “stock loan fee” associated with finding and borrowing the stock can skyrocket. The fewer shares there are to borrow, the higher the cost... sometimes as high a 100% of the value of transaction.

The difference between now and then: Back then, bitcoin had crashed in the wake of the Sam Bankman-Fried fiasco, causing shorts to pile into all things crypto. Miners, already perceived to be on the shadier side of the street, were were natural magnets. Since early on they’ve been embroiled in a number of controversies, including a “web of questionable dealings” dug up by ShareSleuth, which wrote…

Three companies whose stock made big moves last year are linked by undisclosed relationships that raise numerous red flags about the deals that helped attract investors, boost share prices and enrich certain players.

Since then, there has been one accounting controversy after the other, as the Wall Street Journal pointed out in this story...

A look at 19 of the publicly traded crypto miners showed that 16 disclosed significant internal-control weaknesses in the past four years, some of which were “alarming,” according to Bedrock AI, which makes software that analyzes financial filings.

Boosted by Bitcoin

As goes bitcoin, however, so goes the stocks of the miners. This time was no different, with just one twist:

There are the miners, then there’s Marathon, which was the most heavily shorted of all.

In theory, heavily shorted stocks suggest a company might be headed for trouble.

And while there may be comfort in numbers, when it comes to shorts, the more is not necessarily the merrier, since those companies can also be the most squeezable. In other words, as stocks rise, short-sellers often start covering by closing out their positions. That often means buying stocks at higher prices than they borrowed them out.

If prices spike, shorts often panic and start covering more and more shares, creating a feeding frenzy – pushing or squeezing stocks higher. This is no different than what happens with longs when stocks fall, except the lowest a stock can go is zero. The highest a stock can go is, well, infinity... and beyond. That’s why shorting can be so precarious.

Squeezed to High Heaven

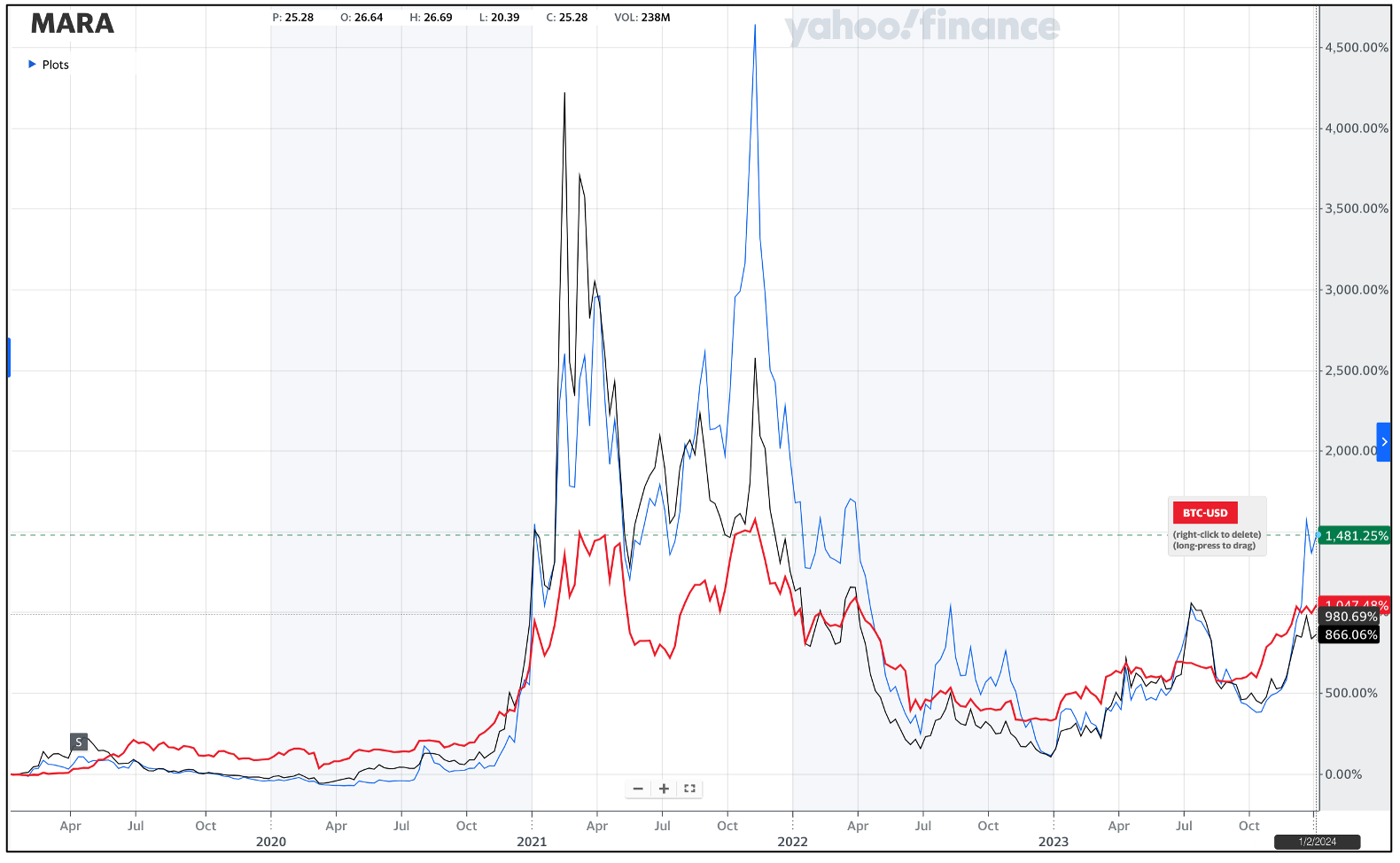

In this case, this chart tells that story....

As you can see, Marathon (blue line) and its chief rival Riot Platforms (yellow), have tended to trade in tandem... often with Riot with better returns.

The same with market cap, where Riot has typically been the bigger of the two.

That all changed at the very tail end of December, when Marathon didn’t just shoot past Riot, but catapulted past it.

Then something else happened...

As those shorts covered into recent weeks, suddenly Marathon’s stock became readily borrowable at no cost. Yet its stock is still roughly 450% to 650% higher than it was when it was impossible to borrow.

Riskier Today?

That gets to the bigger question: Is Marathon, with lower short interest and no cost to borrow, paradoxically riskier to own today than it was back then?

I’m not going to dive into the world of bitcoin and bitcoin miners, instead sticking with the data. As I often do, I checked with the screens from my pals at Kailash Concepts to see how Marathon ranks, quality-wise.

In December, it ranked the 1,547 of 1,547 small-mid cap companies. In other words, at the bottom of the heap… dead last. It also popped up as a “possible manipulator,” with the possible earnings and balance sheet quality after reporting a 671% revenue gain – the biggest in six quarters.

Which brings up something else...

As I was researching Marathon, I scrolled through some posts on SeekingAlpha, including a bearish one from October. As always, I went straight to the comments and was struck by the last line of one comment that was countering the author. It said...

Stop analyzing this company with traditional metrics.

I’ll let the bulls and bears hash out the merits of Marathon’s model, but one thing I do know: when the argument is to ignore traditional metrics, that, my friends is a big old red flag.

Seems if you want to bet on bitcoin, own bitcoin – either directly or through an ETF, if one is approved. After all, other than during outright manias and short squeezes, as the chart below shows bitcoin (red) it has proven to be the safer bet.

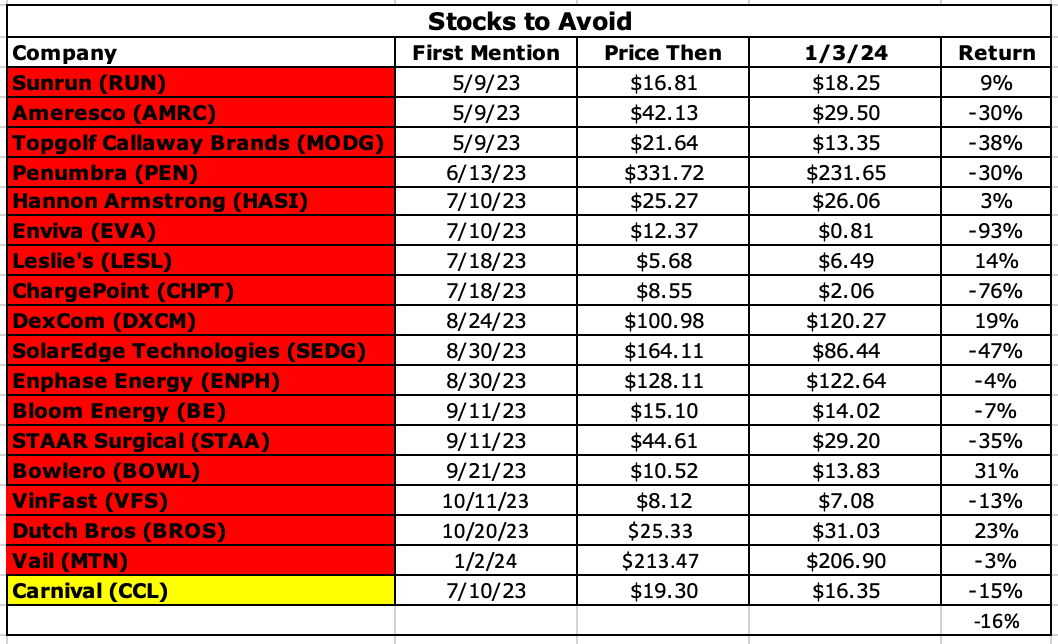

Speaking of Red Flags...

When I started the Red Flag Alert in May, it wound of serving as a proxy for cross-section of potentially risky stocks. At the market’s depths, the group was down an average of well over 30%, with every stock in the red. As recently as early November they were down 32%.

Then came the market’s U-turn, and five of the group – now numbering 18 – zoomed into the green.

As of yesterday, they were down an average of 16%.

As best I can tell, for most nothing has changed from the original thesis. Their declines might have been exaggerated at the lows. Ditto for the velocity of their turnarounds.

Perhaps no company fits that bill better than Bowlero, which is like Marathon was a year ago, with virtually no shares to short. That creates the potential for a squeeze higher – yet nothing has changed from the initial concerns I laid out in “Gutter Ball.”

Also keep an eye on thinly traded VinFast, the Vietnamese auto company. It’s opening dealerships in the U.S., which could tilt the “story” in its favor. I stress story. But then... it still has to sell cars and make money. And given the glutted market for EVs and quite a few horrific reviews – such as this from MotorTrend and this from Car & Driver – that may be one of those Wall Street stories that don’t have happy ending.

DISCLAIMER: This is solely my opinion based on my observations and interpretations of events, based on published facts and filings, and should not be construed as personal investment advice. (Because it isn’t!)

Feel free to contact me at herbgreenberg@substack.com. You can follow me on Threads @herbgreenberg.

Agree with this

“As always, I went straight to the comments and was struck by the last line of one comment that was countering the author. It said...”

I can usually count on the negatives that were glossed over in an article being clearly called out in the comments. People can’t stand to have bad arguments unchallenged. Sometimes those challenges are awful though which is a good indicator an article is on the right track.

Thank you for sharing. Even horse race analysts use data and analytics, although for most of us amateurs hunches, horse names and racing silk colors rule the day. Oh wait, that's why thousands of loosing tickets litter the betting floor.