Red Flag Alert Update – Crossing the Foul Line

Red Flag Alert Update – Crossing the Foul Line

Bowlero strikes again

***Head’s up: Big changes are coming to On the Street. We’re evolving, expanding... reimagining. Stay tuned!***

Dividends are back in vogue, but be careful...

Some companies simply shouldn’t being paying them.

And when they do, especially if they’re loaded with debt, they have negative free cash flow and their financial metrics are going the wrong, it’s an obvious red flag.

When that company owns bowling alleys, and has growing cash needs as it tries to expand through acquisition and new builds, it’s akin to crossing the foul line.

Enter Bowlero ($BOWL), no stranger to readers of my Red Flag Alerts.

I first red-flagged the company in September based on slowing growth, falling margins, rising debt and a business model tied to rolling up an industry that historically has proven to be a lousy investment.

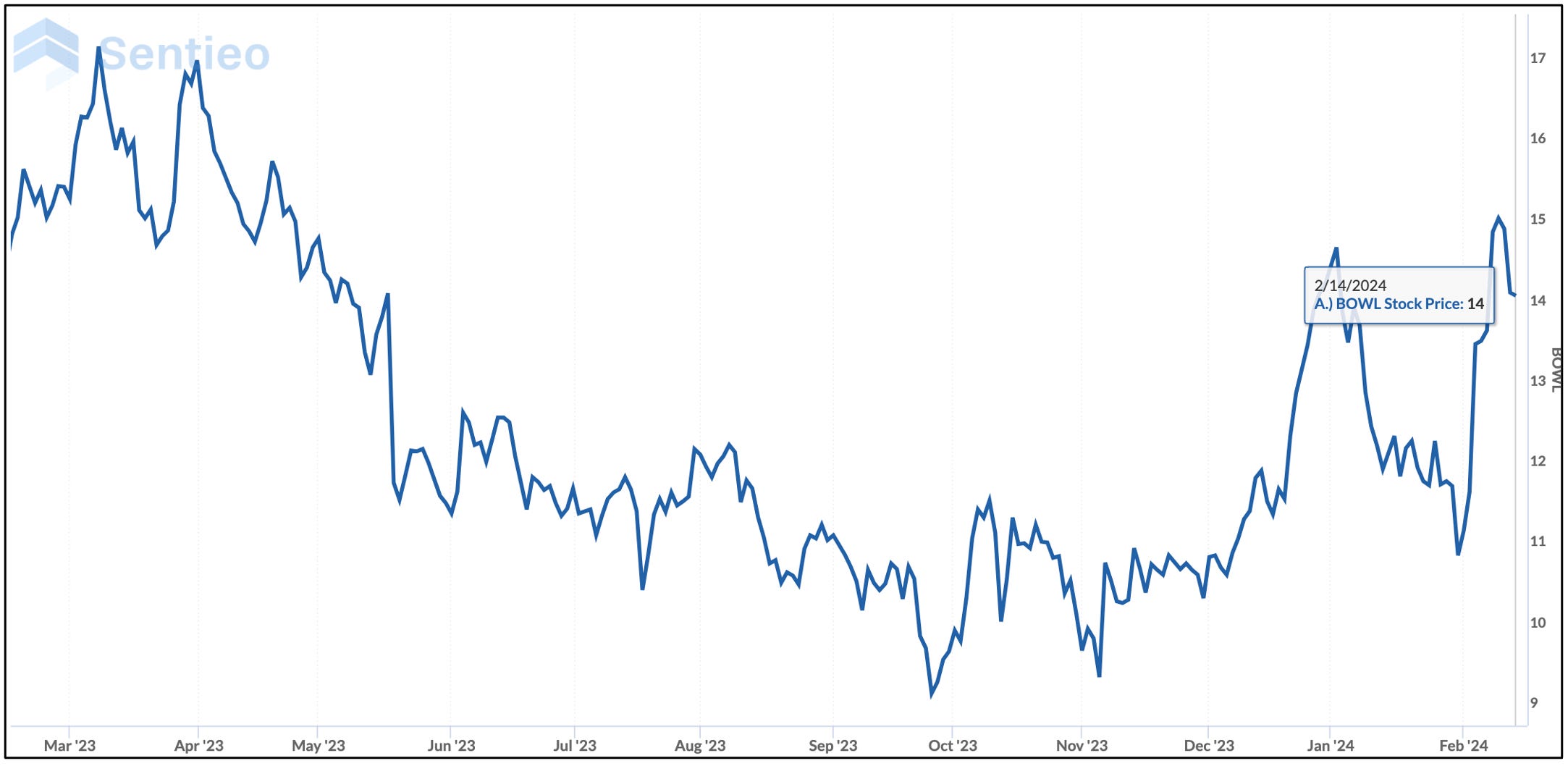

But here we are, five months later. And after its stock had been bobbing around, before recently pulling back it had skyrocketed nearly 40%... in less than two weeks.

It’s not because its business has miraculously reversed itself. It’s because (drumroll!)... it has so much cash not to spend – (sarcasm) – that in addition to actively buying back its shares, it initiated a dividend on its common stock.

Bowlero 101

Before we go further, this quick refresher: Bowlero went public in 2021 as a SPAC. It’s a rollup of bowling alleys. The timing couldn’t have been better…

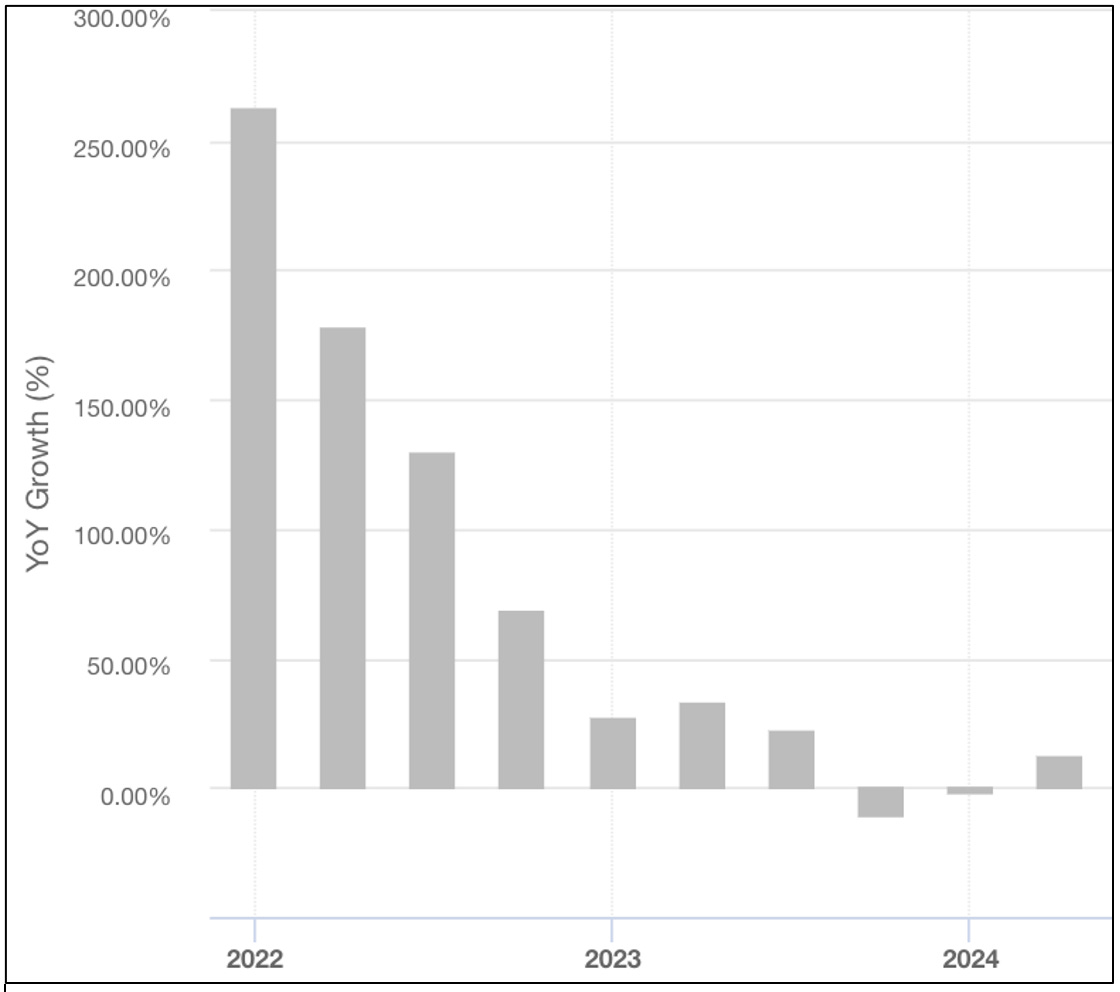

Like similar entertainment-type venues, as lockdowns were relaxed and people wanted to get out, bowling became hot. So hot that booking time at a bowling alley sparked surge-like pricing. Bowlero kept raising prices for no other reason than... it could. Things were going so well that at one point its same-store sales were growing at 30%.

Then came the post-Covid hangover….

Bowling did as it has a history of doing over the decades: As a fad, it faded.

The story is in the numbers. By last October sales were starting to skid, and the company guided to flat-to-down same-store sales...

In the most recently reported quarter it raised prices by a meager 2%, though management also said that included some “low-hanging fruit.”

Here’s the problem, as my friend Katherine Spurlock, a former short-seller, likes to point out...

Bowlero is burning through cash and carrying a mountain of debt. They claim their net debt is $960 million, with a ‘bank credit facility net leverage ratio of 2.5 times.’ (Keyword – bank). But if you throw in those sale-leasebacks, its net debt balloons to $2.6 billion, or a whopping 6.3x of EBITDA.

So, when the company said it’s sitting on a lot of cash ($408 million from recent sale leaseback transactions), and it wanted to reward shareholders – it instituted a dividend– and my jaw dropped.

A Dividend – Really?

With that as the backdrop, we both came to the same conclusion: Why would a company like that pay a dividend? Or in Katherine’s words...

Why the heck would a debt-ridden company seeking to grow its store base by close to 50% pay dividends? And on top of that, why are they buying back shares like there's no tomorrow?

Since going public, they've slashed their share count by a whopping 20% and are currently authorized to repurchase an additional $54 million.

We’re not the only ones wondering about that. On Bowlero’s recent earnings call, one analyst asked...

I’m curious – what made you decide now was the right time to increase capital returns, complementing your buybacks with now you've got this dividend, at the same time you're increasing your investment spending, so maybe you could talk a little bit about your balance sheet.

CFO Bobby Lavan responded...

So I joined here in May and I have been unbelievably impressed by sort of the cash flow generation of this business in the second quarter, third quarter.

We discussed that internally when we looked at all of our different outflows needed over the next few years, M&A, conversions, new builds and we looked at our liquidity and we had ample liquidity to continue buying back stock and pay a dividend.

And so is effectively, we're really excited about where the business is, but we're much more excited about where the business is going and sort of the exit rate on FY 2024 and just the opportunities in the capital. And frankly, there is more capital if we want to bring it in. But right now, we're still sitting on a lot of cash.

It's unclear where that capital is coming from since Bowlero just did a sale-leaseback. It’s equally unclear what he's referring to when he mentions "cash flow generation," since free cash flow is negative, based on the most common definition of operating cash flow minus CapEx.

An Audience of One

What’s more, the company says it has "ample liquidity." That means it has cash on hand to meet short-term obligations. It very well may, but paying a dividend rather than paying down debt would appear to be imprudent and short-sighted, since it does zero to support the business over the long term.

It’s what Lavan said in the very next breath that matters most...

At the end of the day, we're going to reward shareholders and continue to invest in the business.

And when it comes to Bowlero, no shareholder matters more than CEO Thomas Shannon.

With an 85% stake, he’s the single largest shareholder. Any company with a person or group controlling more than 50% of its shares is deemed a “controlled company,” which means it’s exempt from a number of typical corporate governance rules.

As of its last proxy filing in October, Bowlero said that it doesn’t use any of the corporate governance exemptions, adding that at some point it may. But that’s not the point here...

The point is that by declaring a dividend, Katherine reckons that Shannon winds up with an estimated $13.7 million per year, or 42% of the $33 million annual dividend.

And that doesn’t include gains from the rise in the price of his shares, which would appear to have a target of $17.50. That’s the number the stock needs to hit (and stay at or above for 10 days over a 20-day period) so “earnout shares” held by a group led by the SPAC’s sponsor can vest.

The sponsor, Isos Acquisition Corp., is run by Michelle Wilson and George Barrios, former World Wrestling Entertainment co-presidents. They received shares when Bowlero merged with Isos.

Squeeze-O-Rama

The whole earnout picture in this situation is considerably more complicated, but you (hopefully) get the picture. And that gets to a bigger point...

If you didn’t know better – and we certainly don’t – you’d think the dividend was aimed at hoping to create a short squeeze, à la GameStop. Retail investors, after all, love companies and concepts they can grasp. As Katherine explains..

By paying a dividend, Bowlero all but assured that the stock would rocket higher and cause a squeeze, as short sellers must pay the dividend in addition to the cost of borrowing the stock.

And it did... until it didn’t.

After spiking to a high of $15.40 two days ago – looking as though the next stop would be in the $17 range – it’s now bouncing around $14 as I write this.

And this is for a stock that is so heavily shorted there are no more shares to short.

Time to Re-Rack

Therein lies the moral of this story...

Games like these, assuming this is one, work when stocks are going up. But they can backfire if stocks are falling and/or investors are savvy enough to see through any shenanigans.

Plus, as short squeezes go, Bowlero would be puny and potentially more dangerous relative to other highly shorted stocks.

I say dangerous because if the stock really does hit $17.50 and stays there long enough, those earnout shares will automatically vest and presumably convert to common shares. That, in turn, will result in an estimated 7.5% dilution to existing holders. The pressure of the dilution, combined with the likelihood that they would then dump those shares, would undoubtedly cause the stock to tumble.

Then there are the realities of the business, which is trying to juggle the cash needed for potential expansion, with paying dividends and buying back shares. It’s the ultimate in corporate hubris.

Oh, and out of the blue in conjunction with the most recent earnings Shannon shed his title as president, giving it to a longtime insider. He remains CEO, but the question is… why?

I realize that a stock that trades as feebly as this one does can turn in an instant.

And it very well may. But for now, in a market where most heavily shorted stocks are flying, Bowlero looks like a gutter ball.

That’s a long-winded way of saying, red flags continue to fly.

If you liked this, please click the heart button and feel free to your friends.

DISCLAIMER: This is solely my opinion based on my observations and interpretations of events, based on published facts and filings, and should not be construed as personal investment advice. (Because it isn’t!) I do not have a position in this stock.

Feel free to contact me at herbgreenberg@substack.com. You can follow me on Twitter (X) and Threads @herbgreenberg.

I own calls in this stock. Hope my math is decent below.

With all due respect Herb, you are underestimating them. They already have 30M shares in Treasury, soon to be over 40m. With $200M cash they can purchase the entire balance of the float at $9 per share and take the company private. I've never seen anything like this. Then what happens? What about all the mutual funds, other institutions? What about the shorts?

It is totally true that a large insider could dump their stock early and ruin the party- but only a total moron would do that. You are basically saying they are morons and can't manage cash which is why they are buying stock and paying a divi in the first place. I do not think you are correct here. This company could literally squeeze the piss out of these shorts and force them pay off the debt of the entire company.

Regarding the CEO's options, strikes are 15, 17, and 20. I hope no one is working there to see the stock to $25 - they should be aiming at $100.

I'm in, we'll see, I am frequently wrong. Good luck, thank you for the write up, Herb.

I appreciate the analysis here, but I tend to disagree. Clawing back lease payments and tagging that alongside debt doesn’t seem to make much sense when assessing net leverage. All-in it’s accretive to do the sale leasebacks because the lease payments end up being less than the interest payments and they capture more equity by arbitraging the going-in cap rate with the proforma cap rate on the sale when they sell to a VICI with them as a tenant. I also seem to think it’s never a good idea to short a stock that does generate cash both on existing alleys and new alleys (growth capex and maintenance capex should be separated here) with major levers to pull on the ancillary income front (PBA, events, and arcade). Though I agree they’ve pinched the consumer a bit, they have a lot of growth to go in the event space and should generate cash nicely. At this point shorts are kind of stuck and I don’t really see how shares don’t trade into the $17 range until those shares get earned out. The float is tied up and it’s possible the insiders are not lending out their shares. It might be a good short, but not at $13. At $20, we have a different picture though. Full disclosure I’m long a bunch of shares.