Special Report – A Backdoor Play on Longevity

Special Report – A Backdoor Play on Longevity

Danaher makes money, not news

Note: I’ve spent the past two years focused on writing long-biased reports, mostly on companies that are better at making money than making news. All of it behind paywalls. Thanks to a few ch-ch-changes, this one is on the house.

This is the first in a series of “backdoor plays…”

Wall Street almost always takes things too far.

Whenever there’s a new theme or trend, investors are all in...

I’m not just talking about the hottest topic du jour – artificial intelligence, which very well may be overdone, for now, as an investment theme.

There was the Internet boom, when any company not somehow positioned as a dotcom was viewed as archaic and out-of-touch...

Even good ole Berkshire Hathaway (BRK), Warren Buffett’s creation, was relegated at one time to the then irrelevant bucket. Yet to this day, he has one of the most laughably rudimentary websites of any company anywhere...

It doesn’t matter, of course, because its stock has gone on to rank among the most consistently best performers of all.

Then there was the ESG, the acronym for Environmental, Social and Governance. There was a time not long ago that any company not considered ESG-friendly enough was deemed irrelevant to the point of being shunned.

Among them, Allison Transmission (ALSN), which I started recommending back in June 2022 based on the quality of its business. As the largest manufacturer of automatic transmissions for trucks, it gushed free cash flow.

Yet no sooner did I recommend it, than its stock got clobbered, almost as if its shares had been blacklisted.

Its sin: Automatic transmissions for trucks weren’t perceived as being ESG friendly.

Then, as the ESG hype faded, investors rediscovered Allison, whose shares are up 50% since my recommendation.

Which brings us to the latest Wall Street pile-on... or maybe I should say, pile-off...

The impact that Wall Street’s infatuation with those miracle weight loss drugs from Novo Nordisk (NVO) and Eli Lilly (LLY) is having across medtech and healthcare... something I’ve written about quite a bit in recent weeks.

As usual, the selloff is overdone and is creating a good setup for quite a few stocks that were perceived to be in the wrong industry at the wrong time… even if they they’re not.

One of the Best Compounders Ever

Among them – a company that rarely makes the headlines – is Danaher Corp. (DHR).

Danaher’s stock, while slumping, is off considerably less than most. Probably for good reason...

These weight-loss drugs, known as GLP-1s, couldn’t be created and produced without products like those made by Danaher.

Rather than the wrong products at the wrong time, Danaher has right products at the right time with a superb business model against the backdrop of a company that has history of exceptional execution.

If you know Danaher, but haven’t looked at it in years, it’s worth another look.

If you don’t, there’s no shame, because the company has tended to stay out of the headlines even though it’s widely regarded as being among the best businesses, period.

The proof is in its stock, which has been one of Wall Street’s greatest compounders ever... performing even better than Berkshire Hathaway in almost any time period... certainly since Danaher’s founding around 40 years ago.

Started by brothers Steven and Mitch Rales in the early 1980s, Danaher grew out of its real estate roots through a series of junk bond financed hostile takeovers...

It had so much expensive debt that some wondered whether it could ever survive.

Not only did it survive, but it thrived by never standing still... becoming an industrial conglomerate before evolving into other areas, notably healthcare.

‘Constant Reinvention’

Along the way, Danaher has been steeped so deeply in a management philosophy it calls the Danaher Business System that it never lost its way as it transitioned through five CEOs...

Each one put a new spin on the Danaher story.

As the book “Lessons from the Titans” puts it...

The story of Danaher is first and foremost one of constant reinvention.

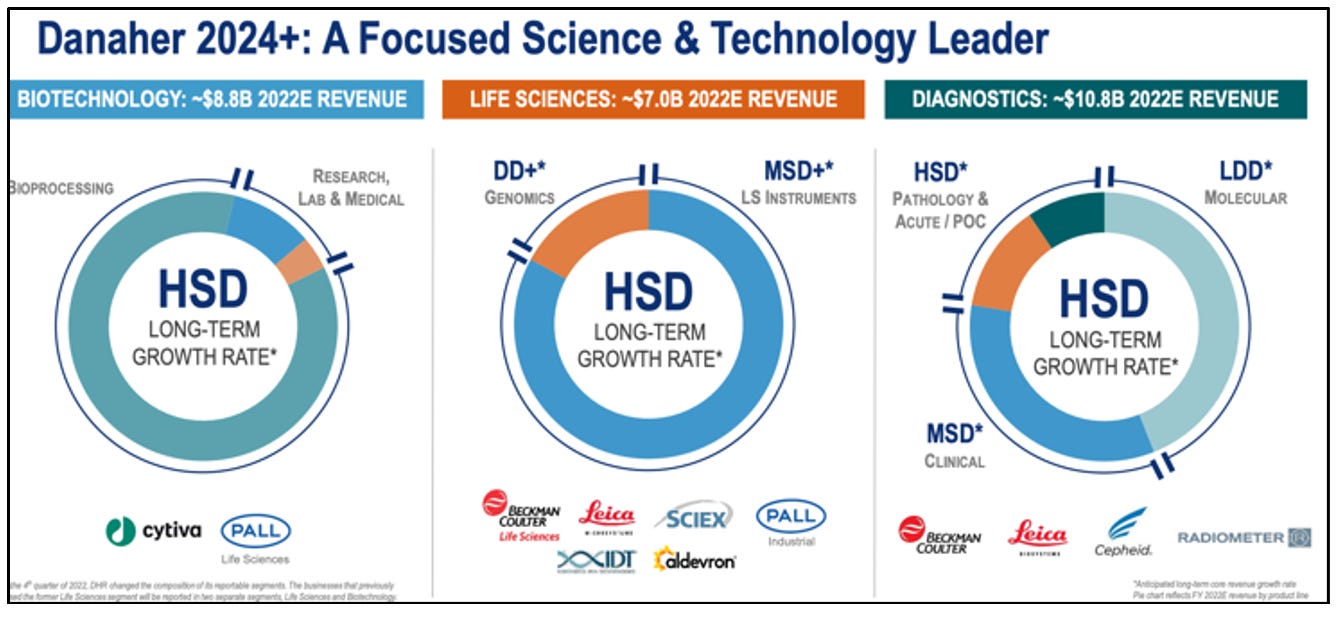

Its latest incarnation, which I call Danaher 5.0, may be its best yet.

With the spinoff of its Veralto water purification business several weeks ago, Danaher has become a pure play on perhaps the most exciting and fastest-growing part of healthcare...

In the company’s words…

We supply the technologies, services and expertise that researchers and biopharma companies need to bring transformative medicines from discovery to delivery.

More specifically, it makes tools, instruments, tests and other types of products that are used in everything from diagnosing diseases to developing and commercializing the biologically derived drugs used to treat them.

Or as CEO Ranier Blair puts it, “A more focused, faster-growing $26.5 billion science and technology powerhouse that is focused on human health.”

It’s a brilliant strategy, and a profoundly positive one at that... with the goal of evolving into what Blair claims will be an even faster-growing and more profitable cash-generating company.

Sticky Customers

To put this in perspective, Danaher converts more than 100% of its profits to free cash flow, which a quarter ago totaled $1.6 billion.

There’s something else...

While management doesn’t come right out and say it, the end result is a company focused on perhaps the single-best investment theme out there... longevity.

The beauty of Danaher’s strategy isn’t just its focus on healthcare, but the way it’s doing it...

Danaher’s business has always leaned heavily on a razor/razor blade business model, which translates into sticky customers and less cyclicality. That, in turn, generates enormous amounts of recurring revenue.

High recurring revenue has always been part of the Danaher story, even back in 2015 when it was an impressive 45%.

My, what a difference eight years and its latest transformation makes...

This year, recurring revenue is expected to be around 75%, hitting 80% next year.

Think about it this way, as Blair explained at the company’s Investor Day last year...

This recurring revenue gives us more touch points and more customer intimacy and more insights into the pain points and the unmet needs of our customers and fuels our innovation engine. And that fuel allows us to develop proprietary higher-margin solutions in order to win additional market share.

That’s especially true for the part of healthcare Danaher is now in...

A Quick Overview

Before we go further, a word of caution: Unless you’re a scientist, which I’m not, if you dive into researching Danaher you’ll find that much of the nitty gritty of its end market will be over your head.

I know... because it’s over mine.

But I also know a good business when I see it, and Danaher is as good as it gets.

The company has three operating segments, but to keep things simple, let’s just say it has two: diagnostics and life sciences.

Diagnostics, on its own, is the biggest, generating 38% of sales. This includes instruments, software and other services and products that doctors, hospitals and labs use to diagnose various diseases.

It’s a rapidly changing and growing industry, thanks largely to the evolution of molecular diagnostics, which uses a genetic code found in our cells to figure out what disease we have. You know those PCR swab stuck up your nose to determine fairly quickly whether you had COVID-19? Yep, you can thank molecular diagnostics.

It currently represents barely a third of the entire diagnostics industry and is viewed by Danaher as having “a significant growth runway,” as molecular diagnostics is used to diagnose more diseases.

Betting on the Boom in Biologics

As interesting as that might be, the real excitement may very well be in the rest of the company...

Especially bioprocessing, where it provides tools and other products used in the development of drugs.

Not just any drugs, but biologics...

Unlike traditional drugs, which are chemically synthesized, biologics are drugs created from living cells.

Today they represent 60% of all drugs being made compared with 20% two decades ago. And as Blair said on the company’s most recent earnings call...

The number of biologic and genomic medicines in development is meaningfully higher than at any point in history.

Biologics are deeply tied to the future of medicine, currently accounting for roughly a quarter of all drugs accepted by the FDA, but represented around two-thirds of all drugs in development... compared with just 33% in 2022.

And while Danaher has competitors – notably among them, Thermo Fisher (TMO), Merck (MRK) and Europe’s Sartorius – no company has the portfolio of bioprocessing products as broad and deep as Danaher.

No wonder bioprocessing is the most profitable and potentially fastest growing part of the new Danaher.

We’re talking the need for all sorts of lab equipment that Danaher makes, and which has to be serviced... a big part of the recurring revenue.

But the bigger part of the story are the various parts required to operate those machines, like filters required for filtration, separation and purification processes; reagents used in diagnostic tests; chromatography resins used for research and bioprocessing; cell culture media used to grow cells; and cartridges for marking and coding equipment.

Crazy Over Consumables

Those are the consumables, which are products that have to be continuously replenished or replaced.

There’s another element of that as well, which management describes as the “turbocharger” of its bioprocessing business: Single-use products, which have already evolved into a $1 billion business for Danaher.

These are used mostly in small batches, which is one of the most promising parts of biologic drugs. That’s because as biologic drugs become more uniquely directed at more limited patient populations, manufacturers can produce smaller and smaller quantities... and still make money.

Think of single-use this way, as Blair explained at an investment conference a few years ago...

The traditional way of manufacturing these drugs was to use big stainless steel vats. So for those of you who like microbreweries, there might be the one or the other of you, that's pretty much what it looks like.

And every time you get done with a batch, you have to go in there with your steam cleaner, steam that out, which you can imagine is a lot of fun.

And then you have to actually validate that you -- that production unit is clean. That's a pretty big headache, and the risk of cross-contamination is pretty high.

And so single-use technologies, literally technologies where you use them one time for the batch and then discard them, are increasingly popular, and they've become more economical as the batch sizes have actually gotten smaller with higher yields.

That’s not to say there isn’t risk, but it’s likely transitional and rolling, tied largely to fits, starts and funding in biologic drug development.

Also worth watching: China, a fast-growing market that accounted for 15% of bioprocessing last year, is likely to shrink to 10% this year, with the drop-off accelerating... thanks largely to geopolitical tensions and lower demand as funding for new drug development there has dried up.

There’s something else at work, too – something impacting Danaher’s customers and competitors... call it the Covid hangover.

The pandemic, as you might guess, was a boom time for the bioprocessing industry. Customers wound up over-purchasing, which has led to bloated inventories on their shelves.

That led to a falloff in demand, which you can see in revenue growth that spiked during the pandemic and is now negative.

As inventories are worked down, demand should start picking up, as should revenue growth... and earnings.

The result should be sharply higher shares in coming years… not weeks or months.

Or as Dan Loeb wrote in his August letter to investors of his Third Point LLC hedge fund, which owns 2.6 million shares…

We would not be surprised to see Danaher’s growth rate move from high single digits to the low teens over time, implying a long runway for Danaher’s business and stock price to increase sustainably while they enable the discovery and manufacturing of key life-saving drugs.

Between here and there, the company’s stock is at the whim of the healthcare “group” and investments in new drug development, which is likely to accelerate.

As Blair explained at an investment conference in May...

As we look at the number of projects in the pipeline, again, we’re talking about thousands of projects in the pipeline, we are as bullish as we have been on the long-term prospects of the industry. And there are many things to look at here that are positives and just reinforce our perspective on the long-term growth rate in this industry.

You all are reading about Alzheimer’s drugs or GLP-1s. These are all exciting things that when they play out, meaning they do need to be approved, they do need to be reimbursed and ultimately prescribed and taken by the patients. But these are all positive indicators on the health of the industry and support our long-term growth view.

Remember, even if they’re not approved, Danaher played a role in their development. Which is what I mean when I say that it has the right products at the right time.

Compete for Shareholders

Danaher also has the right approach to how it runs its business.

Earlier I mentioned something Danaher refers to as the Danaher Business System – the core of its culture and five “values” it lives by. Among them: “We compete for shareholders.”

Normally, I’d be dubious of something like that… thinking it’s just more hollow corporate mumbo jumbo.

But for four decades, Danaher hasn’t just lived by those rules, it has executed on them.

There is no reason to believe this time will be any different.

If you got this far and liked what you read, please click the heart below and please pass the word. Herb Greenberg | On the Street is not published on any specific schedule.

DISCLAIMER: This is solely my opinion based on my observations and interpretations of events, based on published facts and filings, and should not be construed as personal investment advice. (Because it isn’t!) I do not own shares at the time of publication, but may purchase and sell shares without notice.

Feel free to contact me at herbgreenberg@substack.com. You can follow me on Twitter and Threads @herbgreenberg.

Great write up as usual Herb. But what is happening with Empire Real Wealth? I subscribed because of you and now it has a new chief editor and no explanation of what’s going on. Can you share anything about this?

When I read your article the first thing I thought of was Google Deep Mind's Alpha Fold. It's an AI that has already 3D mapped over 200m proteins. They made the database public and say it will be very important to the drug discovery process.

"Hassabis envisions the development of a “virtual cell” that models all cellular dynamics and can be used to perform in silico experiments. This would streamline the research process, requiring wet lab validation only at the final stage."

I don't know exactly what this means but it sounds like the Alpha Fold database may reduce the amount of testing equiptment used in drug discovery. If it does, do you know if this will have a material impact on Danaher's business?

AlphaFold: Redefining drug discovery with digital biology and AI https://www.drugdiscoverytrends.com/alphafold-redefining-drug-discovery-with-digital-biology-and-ai/

DeepMind uncovers structure of 200m proteins in scientific leap forward

https://www.theguardian.com/technology/2022/jul/28/deepmind-uncovers-structure-of-200m-proteins-in-scientific-leap-forward