Special Report – Backdoor Play on AI

Special Report – Backdoor Play on AI

S&P may be boring, but it's also a great business

This is the second in a series of “backdoor plays...”

If you’re like me, you’ve had your fill of anything having to do with artificial intelligence, better known as AI.

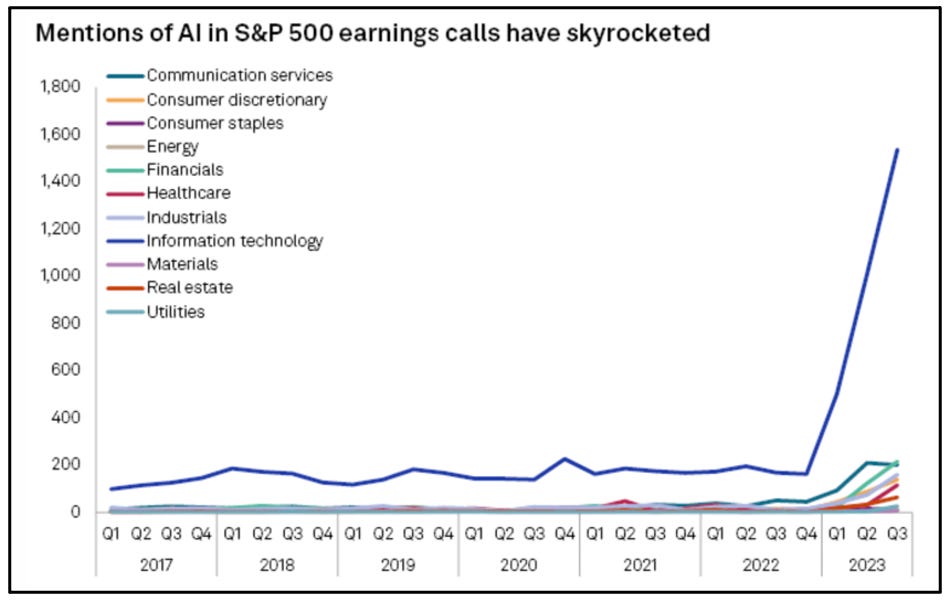

It's everywhere you turn – TV, radio, news articles, investment newsletters, and more. Heck, according to S&P Market Intelligence, the mere mention of "AI" among companies in the S&P 500 Index skyrocketed by 10 times over a year earlier.

Not that AI hasn't been around for years... But the rollout of generative AI, with ChatGPT probably the best-known example, ignited interest and a euphoria not seen since the early days of the Internet.

Before you say you don't want to hear another word about ChatGPT, let me assure you that's not what this is about...

This is about how – as they're evolving – ChatGPT, Google’s Bard/Gemini and other forms of generative AI scrape the Internet for news stories, text, images, audio, and video to build their so-called "large language models," which is where the magic happens.

Much of that is readily available on the Internet, leading some folks to question whether some of what ChatGPT uses violates copyrights.

That’s such an issue that on Substack I clicked a button that doesn’t let generative AI use my copy for training purposes.

If that’s a big issue with text, imagine what it means for data, which supposedly is a big part of the generative-AI story…

No wonder “data” was top of mind during a recent discussion I was having with Matt Ober. (We were actually walking on a path alongside the Pacific Ocean in the San Diego beach town of Encinitas.) He’s a partner at Social Leverage, a VC firm that invests in tech startups.

He knows a thing or two about data…

We first met a few years earlier when he was chief data scientist at the hedge fund, Third Point, which he had joined after being co-head of data strategy at WorldQuant.

When our discussion rolled around to AI, he mentioned that he was actively looking for companies that will somehow springboard off of generative AI technologies...

That led to data, because one thing all of these companies will need, he said, is data. And not just any data, but the good stuff that's mostly behind paywalls.

Extend that to investing, finance, and business in general – and we're talking a need for loads of data... loads of proprietary data.

That led to which companies are best positioned to benefit from the data they own. He mentioned a few, but at the top of the list coincidentally was a company that has for years been a top idea of another friend, who always says the same thing about it whenever we speak: “It’s such a great business.”

A Data Juggernaut

Lightbulbs went off, and I decided to dig in. That’s how I wound up writing about S&P Global (SPGI).

You no doubt have heard of S&P…

The company is best known for its Standard & Poor's credit ratings, as well as its stock indexes – notably, the S&P 500.

What you probably don't know is that S&P is also one of the largest providers of proprietary data – primarily financial, but also on the supply chain, transportation, commodities, environmental, weather, and much more.

No matter how it's spun, while it formally operates in the world of information services, S&P is a data company. It owns enormous amounts of valuable data, either outright or amalgamated, which have been turned into proprietary data sets that would be nearly impossible to easily replicate.

That makes it… a perfect backdoor play on AI.

While the core of its business is steeped in Wall Street, S&P's end markets are a cross- section of corporate America... governments... municipalities... and even farming, mining, metals, banks, insurance, chemicals, biofuels, oil, and mining companies. The list goes on.

Need data on energy carbon capture units? S&P has it.

Battery cell data for electric vehicles? It has that, too.

The history of millions of used cars sold in America? Sure, that's because S&P owns Carfax, which collects the mechanical history on used cars. But S&P also has auto supply chain and marketing data. No wonder it counts 45,000 auto dealers and all major auto makers among its customers.

Data from Day One

Not bad for a company with roots dating back to 1860...

That's when businessman Henry Varnum Poor published a study called "The History of Railroads and Canals of the United States" to give investors data on the growing U.S. railroad industry.

Poor went on to create Poor's Publishing, which published its first credit rating in 1916. Meanwhile, a company called Standard Statistics was creating its own system, and published its first credit rating in 1922.

The two merged in 1941, creating Standard & Poor's. It wasn't until 1957 that the company created the S&P 500.

Nine years later, in 1966, it was bought by financial publisher McGraw-Hill, which owned Business Week and other publications... and ultimately, through a variety of strategically significant transactions, in 2016 evolved into S&P Global.

Turning Point

But the real turning point for the company came a little over a year ago, when S&P acquired IHS Markit for $44 billion...

Even if you haven't heard of IHS Markit, with a price tag that big you have to assume it was an important deal. And it was – turning S&P into the gargantuan data powerhouse that the company is today.

The deal also closed just before the explosion in generative AI, which has sparked a whole new set of problems... but at the same time, it shines a light on the wide moat S&P has built: the value of the data.

As CEO Douglas Peterson made very clear at an investment conference earlier this year...

The No. 1 thing that people like us have to do is protect our data. That becomes absolutely necessary.

We already are very vigilant about our data protection. We have IP lawyers, we file patents. We track down people that are using our information without paying us, etc.

So this is a new place where we'll have firewalls around our data and the usage, as well as in particular products or services that get using our data.

By protecting the data, S&P protects its margins, which are a critically important part of the company's story.

The proof is in the numbers...

From 2013 to 2022, S&P's adjusted operating margins jumped from 33.7% to 45.3%. (In a world where every basis point counts, that kind of gain of more than 1,100 basis points is like winning the lottery.)

And assuming management continues to execute, those numbers are going higher – with guidance of 58% to 60% by 2025 and 2026... on a 69% rise in revenue. Already, the company has been steadily growing revenue...

In this case, I would give management – led by Peterson since 2013 – the benefit of the doubt given how well it has done so far in acquisition after acquisition of valuable data.

It's not just about the data, though... it's the sheer power of S&P's business model that makes it so compelling.

A Closer Look at the Business

While data may be what makes S&P tick, at its core is a subscription business. Subscriptions represent more than half of all revenue, with equally high renewal rates. That translates into recurring revenues higher than an astounding 70%.

All of that is funneled through five business...

1. Market Intelligence,

The biggest of S&P's businesses had an adjusted operating margin of 32.3% last quarter – making it the least profitable of the bunch.

If there was a pure data and data analytics part of the business, this would be it. It's also the part of S&P that's most heavily geared to Wall Street, with various platforms and products, such as Capital IQ, which has been stealing share from Bloomberg and other services. Subscription renewals last year were running higher than 90%, with recurring revenue last year of 95%.

2. Ratings

As everybody knows, S&P rates bonds and other forms of debt

Last year was a tough one, given post-pandemic uncertainties. But near term this arguably is the most compelling part of the story... With $8 trillion in worldwide public debt rated by S&P maturing through 2026 and nearly $13 trillion maturing through 2028, the pipeline for debt needing to be replaced and rerated – resulting in fees – is enormous.

Not just that, this business is also benefiting from something that rival Moody's (MCO) refers to as "bank disintermediation," as companies opt for issuing bonds rather over bank loans, which in turn is leading to whatever well may be a decade-long tail of growth. S&P doesn’t see this as a big part of its future, but it ties into the country’s overall credit dynamics.

There’s also expected to be a boom in private credit markets, as private debt needs to either be securitize or come back into the public markets..

Ratings is also a profitable business, with margins last quarter of 55.4%... It's why Warren Buffett's Berkshire Hathaway (BRK-B) is a long-term investor in Moody's. Ratings, on its own, is simply that good of a business at S&P.

3. Commodity Insights

This is the third-largest segment and is probably perceived as S&P's least sexy business... providing pricing, data, and information for the commodities and energy markets. But what it lacks in sex appeal, it more than makes up for in savvy and sophistication...

Consider that trading of oil or anything energy-related can't be done without knowing the "Platts price," exclusive to S&P through (you guessed it!) a subscription. Like Market Intelligence, Commodity Insights is mostly a subscription business, with recurring revenue of around 90% and an operating margin of 46.2%.

4. Mobility

As the fastest-growing part of S&P, this is one to watch. It's the part of the business that focuses on the auto industry, an evolving business as electric vehicles and online retailing gain traction. This is also the home of Carfax. Last quarter, margins came in at 39%.

5. S&P Dow Jones Indices

Finally, this is the smallest but most profitable part of the company – with margins of 68%.

This unit manages all S&P and Dow Jones stock indexes – having launched the first, with the S&P 500, in 1957... and in 1976, the first index-based mutual fund with the Vanguard 500. It was also the force behind the first U.S. exchange-traded fund ("ETF") in 1993.

Even after all these years, and so many ETFs and indexes, this business continues to grow as so-called passive investing continues to grab share from active managers. S&P earns a fee based on assets under management on all funds using one of its indexes. Blackrock, Fidelity, State Street... they all pay fees to S&P. As one friend puts it, "it's the ultimate toll booth."

Putting It All Together…

Therein lies the beauty of this...

With management forecasting organic revenue growth of between 7% and 9% and low double-digit earnings growth over the next two to three years. The company has great free cash flow ("FCF") – much of which is paid out in buybacks and dividends, which have been steadily ratcheting higher for years.

Based on those dynamics alone, S&P is a solid investment.

Add in the data and combine it with AI, and that's where things get even more interesting...

We all have AI fatigue, but sometimes the time of peak pain is the point when you need to focus the most... it's when the real opportunities start to present themselves.

Ahead of the Curve

And when it comes to AI, S&P has been well ahead of the curve…

Often overlooked in the S&P story is Kensho, an AI company S&P bought in 2018 for $550 million.

Like IHS Markit, you probably haven't heard of Kensho... but I like to think of it as S&P's secret weapon. The company refers to it as "an innovation accelerator."

Long before ChatGPT was on the tip of everybody's tongue and AI was the craze to beat all crazes, S&P had already been focused on combining AI with data.

It had actually partnered with Kensho years earlier, so it was already well ahead on how generative AI – and the so-called "large language models" – was likely to evolve for its end markets.

Or as S&P’s outgoing CFO Ewout Steenbergen put it at an investment conference earlier this summer...

We are in an inflection point, what is happening with artificial intelligence. Because no one really had foreseen the power of those large language models. And that is effectively coming up over the last year or so that this really has accelerated. I see this really as a game-changer not only for our industry but in general. It's probably the kind of a moment similar to the introduction of Internet.

Because those large language models are so powerful, what they're able to accomplish, and the developments are going so quickly that it will be really transformational in many different ways.

At another conference a few days earlier, CEO Peterson added that while the company doesn't have the capital "to invest to build a really large language model" on its own, he quickly added...

But we do have the data.

Indeed, while it's still early in the game, various possibilities are starting to emerge...

On one hand, that data combined with the likes of ChatGPT can help cut costs internally. While bots can't think and can't replace people when it comes to analyzing management, they can certainly cull through the data – the kind S&P owns – and generate reports... This expedites the process, and with fewer analysts.

On the other hand, there's the potential monetization of the data. S&P currently says in a comment on its second-quarter earnings presentation that its data "will not be made available for independent commercialization by third parties or customers."

That doesn't mean it never will, especially if growth ever slows. After all, the data is the data and as Peterson said, "We do have the data."

And as we all know, everything is for sale for a price.

Now for the Risks…

As for risk, every company has risk – as does S&P, especially cybersecurity given the immense amounts of critical data it owns. It also has regulatory risk... that maybe it controls too much data.

That last part may sound far-fetched, but never ever forget that after the financial crisis, when the credit-rating companies were sued by the U.S. government for their role in mis-rating mortgage-backed securities that led to the great financial crisis. S&P, for its part, wound up paying fines of more than $1.3 billion... but ultimately survived efforts by regulators to shut down the ratings industry.

If that’s the worst-case scenario, anything else is likely to be transitory.

As for the Stock

At its current price of $415 per share, S&P Global has a market capitalization of $123.2 billion... and it trades at around 28 times next year’s expected earnings.

That’s not cheap, but it has traded at somewhere between 25-35 times earnings... all the way up.

It currently trades at around 24 times 2025 estimates.

As a friend who has been long S&P on and off for years explains...

It’s not a bargain, but it’s capital light – the most capital light company in information services. And it has cyclical leverage because of the potential for an increase in bond issuance. Its margins will improve and its. Still working on revenue synergies from its IHS Markit acquisition. And they’re investing their cash flow into buying back stock.

His strategy has been to sell at 30 times earnings and buy it back at 20 times.

Right now it’s in the middle of that range. And that's as the company is just beginning to scratch the surface of monetizing AI... and before a coming tsunami of debt refinancing hits.

The headline here is a “backdoor to play AI,” but in truth S&P is a direct play on data, the markets and, more broadly, the entire financial world.

Boring? Sure, but as a business, that’s as good as it gets.

If you liked this, please don’t hesitate clicking the heart button below… and please tell your friends and neighbors.

DISCLAIMER: This is solely my opinion based on my observations and interpretations of events, based on published facts and filings, and should not be construed as personal investment advice. (Because it isn’t!) I do not own shares at the time of publication, but may purchase and sell shares without notice.

Feel free to contact me at herbgreenberg@substack.com. You can follow me on Threads @herbgreenberg.

Some of S&P's data products such as Compustat for financial statement data are collected from public filings, such as SEC 10K, 10Q, 8K filings. Do you think the AI disruption would narrow the gap between it and any less (human-)resourceful competitor in the data vendor space?

As usual, Herb provides thoughtful information! Way to go, young sir!